featured integrations

ACH PAYMENT OPTIONS

Pay-Ins | Payouts | One Platform

Payment solutions

ACH Solutions That Work for You

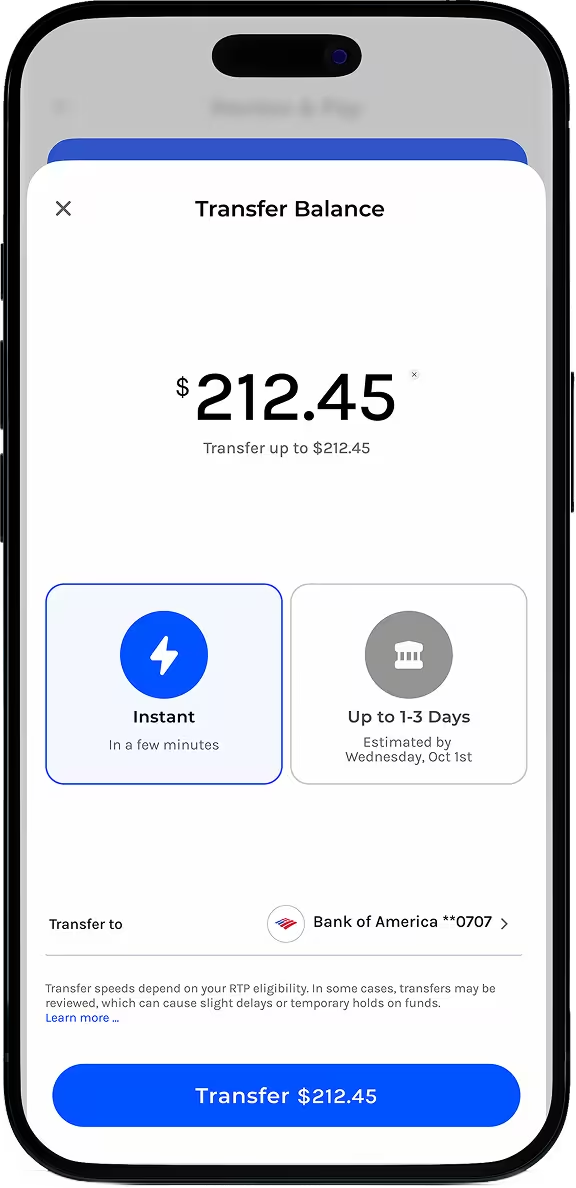

Whether you prefer traditional ACH or Plaid-verified payments with real-time balance checks and built-in risk scoring, Paynote gives you the flexibility to optimize approvals, reduce returns, and scale with confidence.

.avif)

What we offer

Modern ACH Payments

Give your customers more ways to pay—and get paid faster. Paynote makes ACH seamless with real-time verification, instant payouts, and built-in risk controls powered by data.

How to get started

Get Approved Today

1

Connect with a payments expert to align on your use case and integration.

2

Complete a simple application and securely submit your documents.

3

We review your account and provide a clear decision -fast.

4

Our team deploys your account-so you can start processing payments right away.

Industries

Who we serve

Trusted by business owners

“Best In The Game”

“Five stars”

“Best Processing Company Out There”

“I 100% recommend Paynote”

“God level payment partner”

“Very happy about working with Paynote ... ”

“10/10 service and super fast”

“Fast, responsive, and on point”

“With Paynote Since 2024”

“3 years in and no complaints”

“Fast, Reliable, and absolutely Paynote"

“Approved instantly”

“Excellent onboarding experience”

“Paynote saved us from a 90-day Stripe hold”

“Paynote is the BEST”

featured integrations

You have questions, we have answers

ACH Processing FAQs

What is ACH payment processing and how does pay-by-bank work?

ACH payment processing (Automated Clearing House) allows businesses to accept payments directly from a customer’s bank account. Pay-by-bank modernizes this flow by enabling users to securely connect their bank via credentialed login instead of manually entering routing and account numbers.

With platforms like Paynote, businesses can offer ACH across checkout, invoices, subscriptions, and payment links through a single integration—creating a faster, more reliable payment experience.

How do pay-ins and payouts work with ACH and real-time payments (RTP)?

Pay-ins refer to collecting funds from customers, while payouts involve sending funds to vendors, partners, or users. ACH is commonly used for pay-ins, while RTP (Real-Time Payments) enables instant payouts directly to a bank account.

Modern payment platforms combine both—allowing businesses to accept ACH payments and then push funds out instantly via RTP or expedited ACH, all within one system.

What are instant payouts (RTP) and how fast are they?

Instant payouts use RTP rails to transfer money between bank accounts in real time—typically within seconds and available 24/7.

This is ideal for use cases like gaming withdrawals, marketplace payouts, or contractor payments. When RTP isn’t available, expedited or same-day ACH can be used as a fallback to ensure fast access to funds.

How does ACH checkout improve conversion rates?

ACH checkout reduces friction by eliminating the need for card entry and minimizing payment failures. With pay-by-bank solutions powered by providers like Plaid, customers can connect their bank instantly and approve payments in just a few clicks.

This streamlined experience helps increase conversion rates, especially on mobile, while also reducing cart abandonment.

Can ACH payments be used for subscriptions, invoices, and payment links?

Yes. ACH is widely used for recurring billing, invoicing, and one-time payments via payment links. It’s especially effective for subscriptions due to lower failure rates compared to cards.

Modern solutions allow businesses to manage all of these payment types—subscriptions, invoices, and links—through a unified system and API.

How long do ACH payments take to process and settle?

Standard ACH payments typically settle within 1–3 business days. However, many providers offer expedited funding options, including same-day ACH or faster access to funds.

Some platforms also combine ACH with instant payout capabilities, allowing businesses to shorten the time between receiving and distributing funds.

How does ACH reduce payment declines compared to credit cards?

ACH payments pull funds directly from a customer’s bank account, avoiding common card-related issues such as expired cards, insufficient limits, or issuer declines.

This leads to higher approval rates and more reliable payment performance, particularly for recurring or high-value transactions.

Is ACH payment processing secure?

Yes. ACH payments use bank-level security and are often enhanced with tokenization and credentialed authentication through providers like Plaid.

Advanced platforms also include bank verification and risk scoring tools to help detect and prevent fraud before transactions are processed.

What are ACH returns and how can businesses reduce them?

ACH returns occur when a payment fails after submission—often due to insufficient funds or authorization issues. While ACH doesn’t have traditional chargebacks, returns still present risk.

To reduce returns, businesses can use tools like bank account verification, risk scoring (e.g., Plaid Signal), and return management workflows to filter high-risk transactions.

Do I need multiple integrations for ACH, checkout, and payouts?

No. Modern payment platforms, like Paynote, offer a single integration that supports ACH payments, card processing, checkout flows, invoicing, payment links, and payouts (including RTP).

This unified approach simplifies development, reduces operational complexity, and provides better visibility into the full payment lifecycle.